Section 12E of the Income Tax Act was created specifically to encourage new business ventures and to create jobs and this encouragement comes in the form of reduced taxation for qualifying small businesses.

It is critical for the entrepreneur and small business owner to understand how to structure his/her business in order to qualify for this reduced tax benefit.

Please note that this section is not intended to benefit any professional person who renders his/her personal services through a company or close corporation.

What is an SBC?

Personal services entities who maintain at least three full time employees for core operations would qualify as an SBC. It is important to note what is defined as a ‘personal service’.

The first category includes professional or semi-professional activities that require a particular qualification and in many cases a license, certificate or membership of a professional body in order to practise. Examples here would include accounting, architecture, education, engineering, law, health and real estate.

The second category comprises broadcasting, commercial arts, entertainment and sports.

Qualifying criteria for SBC

Currently, a Small Business Corporation (SBC) is defined in the Act as a close corporation, co-operative or private company, where the gross income does not exceed R20 million per annum and which complies with all of the following requirements:

- All the shareholder/members must, at all times during the year of assessment, be natural persons (i.e. individuals and not other companies)

- Shareholders/Members may not hold any shares/member’s interest in the equity of any other Company/Close Corporation. A share/interest in a listed company, collective investment scheme, friendly society and less than five percent holdings in certain other corporations would be exempted from this clause.

- Not more than 20% of the gross income and capital gains consists of investment income and income from the provision of professional/personal services. Investment Income would include interest, rental income, royalties, dividends and trading in fixed property and marketable securities.

What is the benefit?

The best way to explain this is by way of example.

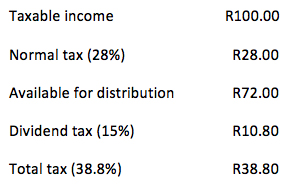

The effective tax of a resident company (excluding a personal service provider) that is assumed to pay out all profits as dividends is calculated as follows:

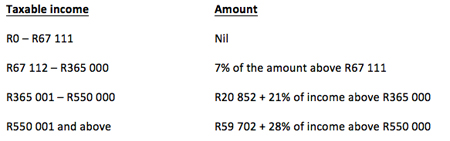

The rates of tax levied on an SBC for years ending between 1 April 2013 and 31 March 2014 are as follows:

If we assume that your business makes taxable income of R600 000 for the 2014 tax year the following tax would apply:

This results in a tax saving of R232 800 less R84 757 = R148 043. This is a massive saving for a new business that would typically be battling with cash flow issues.

Over and above these normal income tax savings, SBCs also qualify for accelerated wear and tear allowances as well as Capital Gains Tax relief.

It is strongly advised that small business owners and entrepreneurs consult a tax professional, experienced accountant, lawyer or Chartered Accountant that is familiar with the Income Tax Act to help advise them on company structure in order to take advantage of the tax benefits that are available to them.

This may not be as daunting as it sounds as there are companies on the market that offer this kind of service on a part time or project basis.