Here are 20 secrets to wealth creation that millionaires aren’t sharing with you

Millionaires have particular habits and strategies in their daily lives that result in them becoming wealthy.

There are 46 500 millionaires, 2 060 multi-millionaires and 639 ultra-high net worth individuals (+ 30 million) in South Africa, according to Knight Frank’s Wealth Report 2016. This shows that more people are figuring out how to achieve financial freedom, but the question remains; how are they doing it?

Spend less than you earn

Over the long run, you’ll be better off if you strive to be anonymously rich rather than deceptively poor.

“Financial peace of mind isn’t the acquisition of stuff. It’s learning to live on less than you make, so you can give money back and have money to invest. You can’t win until you do this,” says Dave Ramsey, an American businessman, author, radio host, television personality, and motivational speaker.

The more money you don’t spend the more you can accumulate and invest, and turn into passive income, which in turn will grow your wealth.

Keep your focus

You won’t become a millionaire overnight, so you’ll need to keep your focus and remain patient until it happens.

“If you took our top fifteen decisions out, we’d have a pretty average record. It wasn’t hyperactivity, but a hell of a lot of patience. We stuck to our principles and when opportunities came along, you pounced on them with vigour,” says Charlie Munger, vice chairman of Berkshire Hathaway.

Numerous millionaires make it to their end goal by saving and investing, and slowly over time they become millionaires. Patience and focus can help you achieve your wealth goals.

Weigh-up value versus worth

The reason people are reaching millionaire status is because they aren’t buying the flashy cars and the fancy houses. They’ve learnt from Warren Buffett’s example and they still live in the same house and they still drive ten-year-old sedans.

“Too many people spend money they earn to buy things to impress people that they don’t like,” said Will Rogers, a stage, motion picture actor and social commentator.

It takes a particular type of person that doesn’t care what people think, and is focused on their goal to forgo spending money to impress others.

Pay off your monthly debts

As any financially savvy person knows, no matter how much you earn, if you still have debt it’s going to eat away at your income.

“The only way you will ever permanently take control of your financial life is to dig deep and fix the root problem,” says Suze Orman.

It may not feel like you’re moving forward by paying off your debt, but once it’s gone everything extra you make can start earning interest and growing your wealth.

Money will never buy happiness

Money does allow you to achieve financial freedom, but remember: “There are people who have money, and there are people who are rich,” says Coco Chanel. Money can provide an easier life, but that should not be mistaken for happiness, you’ll need something else to drive you to achieve millionaire status.

“Happiness is not in the mere possession of money; it lies in the joy of achievement, in the thrill of creative effort,” Franklin D Roosevelt said.

Financial freedom is a mind-set

Financial freedom is a state of mind that comes from being debt free, which you can attain regardless of your income level.

“Financial freedom is a mental, emotional and educational process,” says Robert Kiyosaki.

You need to have the right mind-set to achieve the millionaire status or you won’t make it to the finish line. When you have no debt, you can take more risks.

“Every risk is worth taking as long as it’s for a good cause, and contributes to a good life,” adds Richard Branson.

Have multiple sources of income

Getting a second job not only increases the size of your income, but also keeps you busy, and a busy person doesn’t have time to spend the money they already have. Never depend on a single income. Make investments to create a second one,” says Warren Buffett.

On the other hand, if you aren’t knowledgeable in the stock market, then perhaps start your own business on the side.

“The best thing you can do is start a home-based business,” adds Dave Ramsey.

Manage your money to attain growth

You can’t expect your money to grow and mature if you aren’t using some form of credible money management.

“The single biggest difference between financial success and financial failure is how well you manage your money. It’s simple: To master money, you must manage money,” says T Harv Eker.

Without financial management, your money isn’t going to do anything, you need to be proactive and work your money every day to ensure maximum growth.

“If you look at the average amount of money you will earn over your lifetime, and figure out how many years you are working, most people earn more than a million dollars over their working life, but very few people become millionaires,” says Nancy Butler, a certified financial planner.

“How they manage what goes through their fingers usually makes the difference.”

Pay yourself first

Paying yourself is an essential strategy of personal finance and a great way to build your savings and instil financial discipline.

“Paying yourself first means saving before you do anything else,” says David Blaylock, a financial planner.

“Try and set aside a certain portion of your income the day you get paid,beforeyou spend any discretionary money. Most people wait and only save what’s left over — that’s paying yourself last.”

Paying yourself first will allow you to grow your wealth and increase your principle investment every month.

Have a passion for your work

People say you have to have a lot of passion for what you’re doing and it’s totally true. The reason is because it’s so hard to succeed in business that if you don’t, you might give up. You have to do it over a sustained period of time. So if you don’t love it, if you’re not having fun doing it, you don’t really love it, you’re going to give up. And that’s what happens to most people.

If you really look at the ones that ended up being ‘successful’ in the eyes of society and the ones that didn’t, oftentimes it’s the ones who were successful that loved what they did, so they could persevere when it got really tough. And the ones that didn’t love it quit because they’re sane, right? Who would want to put up with the stuff if you don’t love it?

“So it’s a lot of hard work and it’s a lot of worrying constantly and if you don’t love it, you’re going to fail,” said Steve Jobs.

Don’t underestimate a well thought-out plan

As the saying goes, if you fail to plan, you’re planning to fail. Millionaires that reach this milestone without a plan, usually, get there through luck, and what are the odd that’s going to be you?

“The reason most people never reach their goals is that they don’t define them. Winners can tell you where they are going, what they plan to do along the way, and who will be sharing the adventure with them,” says Denis Waitley, Human Achievement Expert.

It’s not enough to declare that you want to be financially free; you have to work out every step to get there.

Set big hairy audacious savings goals

Don’t be afraid to think big when setting your savings goals.

“If you always do what you’ve always done, you’ll always get what you’ve always got,” said Henry Ford.

Don’t be afraid to really go after what you want even if it’s hard, or you’re uncertain you can make it.

Financial success demands that you have a vision that is larger than you can currently deliver on.

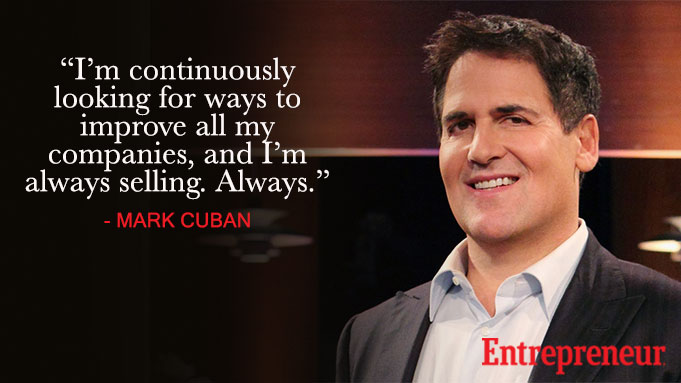

Work harder than anyone else

Hard work can often help to make up for a lot of financial mistakes throughout your journey to success, and you will make financial mistakes.

“I still work hard to know my business. I’m continuously looking for ways to improve all my companies, and I’m always selling. Always,” says Mark Cuban.

Hard work can literally set you apart from your competition and help you to reach your goal faster.

“There is no such thing as overnight success or easy money. If you fail, do not be discouraged; try again. When you do well, do not change your ways. Success is not just good luck: It is a combination of hard work, good credit standing, opportunity, readiness and timing. Success will not last if you do not take care of it,” says Henry Sy, Sr.

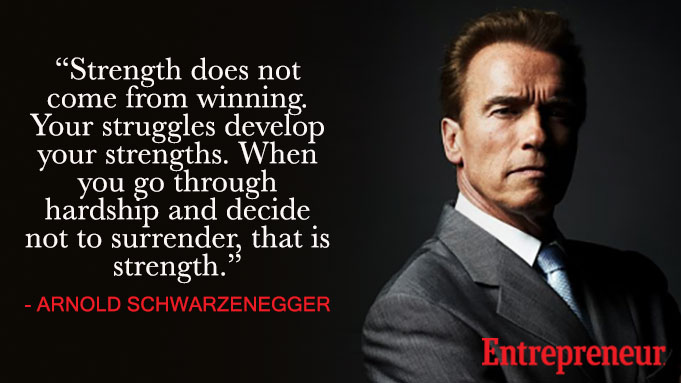

Ensure your long term success by insuring yourself

Bankruptcy is a reality and can come for you at any time. It can be triggered by variables including: Death, divorce, disability or even a poor investment.

“If you have made mistakes, even serious ones, there is always another chance for you. What we call failure is not the falling down, but the staying down,” says Mary Pickford.

When you insure yourself against risk it gives you time to course correct and save your future.

“Strength does not come from winning. Your struggles develop your strengths. When you go through hardship and decide not to surrender, that is strength,” says Arnold Schwarzenegger.

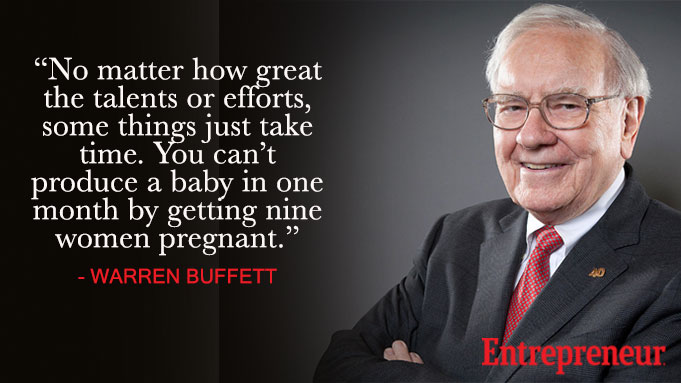

Time is most precious

If you begin saving in your twenties, you can take maximum advantage of the power of compound interest for your savings.

“No matter how great the talents or efforts, some things just take time. You can’t produce a baby in one month by getting nine women pregnant,” says Warren Buffett.

Remember that you’re playing the long game, and sometimes the only way to achieve millionaire status is to keep doing what you’re doing for long enough.

Keep your money hidden from you

You can’t spend what you can’t see. You should use debt orders to pay your retirement and other savings accounts. As your salary increases, you can painlessly increase the size of those deductions to ensure you put money aside every month.

“If you want to get rich, you’ll need to save what you earn. A fool can earn money; but it takes a wise man to save and dispose of it to his own advantage,” says Brigham Young.

Pay off your large scale debt

Once you’ve paid off your house and any other large scale items, you can direct those payments into your savings as well.

“To acquire money requires valour, to keep money requires prudence, and to spend money well is an art,” says Berthold Auerbach.

Ensure you’re spending your money on what really matters and not just the interest on your debt.

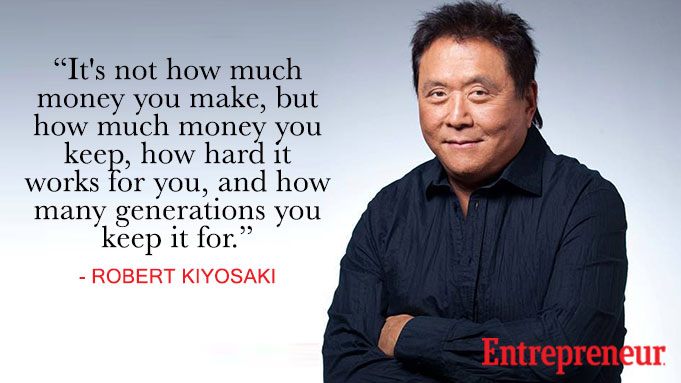

Your salary’s only half the story

Climbing up the corporate ladder will only get you so far, eventually you will have to make your money work hard for you.

“It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for,” says Robert Kiyosaki.

Generating income from passive, rather than active, income sources is the best way to do this.

Timing isn’t (always) everything

No one can really predict the market; in order to be wealthy you can’t moonlight as a day trader.

“Time [period] is more important to investment success than timing,” explained Peter Lazaroff, a financial planner.

“Most of the population believes that timing the market’s moves is the key to growing rich through the stock market. The wealthy, however, understand that time and compound returns are the most important factor in growing wealth.”

Achieving millionaire status requires investors to adopt a buy-and-hold strategy, ride out market fluctuations and ignore rumour and speculation.

Value vs cost: Understand the difference

Paying for consultants to give you insights into growing your wealth shouldn’t sound counter-intuitive, especially if this isn’t your area of expertise.

“The wealthy person has three best friends: Her attorney, her accountant and her adviser. The wealthy tend to use the law and tax code to their advantage when figuring out how to maximise their wealth, especially over multiple generations, and they are not afraid to spend money up front for counsel to get these answers,” says Justin Kumar, a portfolio manager.

“The wealthy look at value over cost, but they are still prudent in their decisions.”