By Dave Mohr, Chief Investment Strategist, and Izak Odendaal, Investment Strategist at Old Mutual Multi Managers (OMMM).

Monday’s rare supermoon – where the moon will be the closest to the earth at any point between 1948 and 2034 – appears to be the apt metaphor for this year’s string of unlikely events. Some will say it started when the odds on Leicester City winning the English Premier League went from 5000/1 to 1/5 in May.

Then Brexit happened, the United Kingdom’s withdrawal from the European Union membership, followed by Donald Trump’s election as president of the United States.

As unlikely as his candidacy seemed a year ago, he clearly tapped into some of the same anti-immigration, anti-globalisation and anti-establishment discontent that drove the Brexit vote.

It is ironic, since the UK and US economies have outperformed most other developed countries since 2009, and have relatively low unemployment. Crucially, though, both have higher income inequality. Looming elections in Europe – Italy, Austria, the Netherlands, France and Germany –will have key votes over the next 11 months, and these will now draw much closer scrutiny.

There is clearly unhappiness with the liberal global economic order that has been in place since the fall of the Berlin Wall in 1989.

Limited market fall-out so far

Despite being a shock, the Brexit vote had little lasting impact on markets (apart from the pound, which remains very weak). As it became clear during the night that Trump would win, the immediate market reaction was a sell-off on Asian equity markets, a plunge in the Mexican peso (Mexico is heavily reliant on free-trade access to the US economy), and falling US equity futures.

However, by the end of the day US equities closed higher, reversing the early losses. The following day, Asian equities rebounded sharply. As with Brexit, this cautions against a knee-jerk reaction to unexpected events. Few predicted a Trump win, but those who did warned of a market correction.

This hasn’t happened, and illustrates why it is so difficult to build portfolios around specific events where the outcome is uncertain even if the timing is known (elections, referenda, ratings announcements). Sensibly diversified portfolios are still better than concentrated fearful ones.

The US is of course a much bigger economy than the UK, and what happens there truly has global implications. Trump’s campaign promises to block immigration and tear up trade agreements would be negative for the US and the global economy. On the plus side, he also promised to upgrade US infrastructure. US government infrastructure spending as a percentage of gross domestic product is close to a 60-year low.

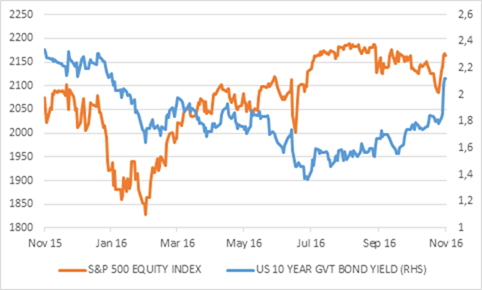

By the end of the week, US and other developed equity markets were up strongly. The equity market is therefore pricing in a stronger economy and more business-friendly economy (with lower taxes and less regulation) under a Trump presidency.

However, the longer-term implications are unknown until we have a better idea of what his policy proposals are and if he will get backing in Congress.

Fed outlook

As far as the global economy and markets are concerned, the most important building in Washington, D.C for now is not the White House but the Federal Reserve’s Eccles building four blocks to the South West.

Aggressive interest rate hikes are much more likely to cause a US recession and deep bear market than Trump’s policy changes. The likelihood of a rate hike in December implied by futures markets fell from 80% to 50% on the election news, but have risen since.

Barring a change in the underlying economic reality, the Fed is still expected to hike interest rates gradually without upsetting the markets or the economy.

Since the Trump campaign attacked the Fed for its failure to raise rates, the longer-term outlook is unsure. However, the Fed is an independent institution with a mandate from Congress to achieve stable prices and full employment. Also, Janet Yellen will stay on as Chair until 2018 and will remain a board member until 2024.

Therefore, abrupt monetary policy changes are unlikely, but it does appear that there might be a shift in emphasis away from using low interest rates to stimulate the economy to using fiscal policy (tax cuts and government spending).

This would be welcome and is exactly what many prominent economists were calling for (ironically, most of them were also stridently anti-Trump). However, it also implies more government borrowing and potentially higher inflation and therefore upward pressure on bond yields.

This is clearly what the market sees: The US 10-year treasury yield rose above 2% for the first time since January. However, this could be an overreaction, since no-one knows exactly what Trump’s plans are yet.

What does all this mean for us in South Africa?

To continue with our metaphor, the supermoon is expected to result in extreme tides. As much as we grapple currently with political uncertainty and the fall-out from policy own goals, South Africa’s history also points to the influence of big global tides on our economic shores, specifically on commodity prices, sentiment towards emerging markets and global capital flows.

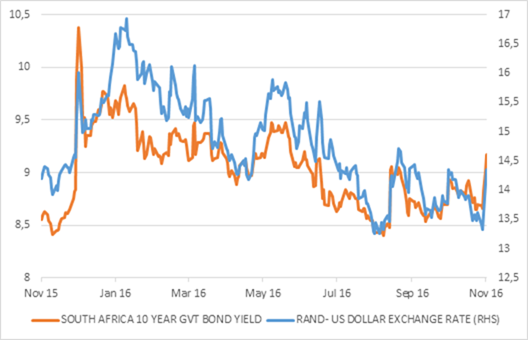

Typically the risk is always there that the heavily traded rand sells off with negative consequences for the local inflation and interest rate outlook. The rand lost 5% against a US dollar that firmed against most currencies. However, the rand had strengthened quite a bit prior to the election.

On the positive side for the rand, commodity prices have firmed up this year as China’s economy seems to have picked up some speed (with the key manufacturing gauge in positive territory again).

There are concerns that the US could hike tariffs on Chinese imports, but starting a trade war with the world’s second largest economy would be an extreme move even for Trump.

China can also hardly be called a currency manipulator when the falling yuan is accompanied by falling, rather than rising, foreign exchange reserves. It is clearly capital flows rather than government buying of dollars that has pushed the yuan to a six-year low.

More infrastructure spending in the US could also be positive for commodities. Trump has promised to dial back America’s commitment to fighting climate change, which is supportive of coal and energy producers, but obviously bad news for the environment.

However, sentiment towards emerging markets has taken a knock, given their general reliance on trade. South Africa’s preferential access to the US market under the African Growth and Opportunity Act (AGOA) was recently secured until 2025.

No African country makes it into the top 30 list of US trading partners and there is no reason to expect any anti-trade backlash against AGOA.

Moreover, while the US is an important export market for us, South Africa exported more to the BLNS countries (Botswana, Lesotho, Namibia and Swaziland) than to America in 2015. China was our single biggest export destination. However, other emerging markets are very dependent on exporting to the US.

Finally, capital flows are greatly influenced by the risk-free rate – if US Treasury yields rise further, it could place pressure on the rand and local rates, and higher yielding emerging market assets in general. However, if US yields are rising on hopes of faster growth, that would also be a good sign for the global economy.

Chart 1: Impact on US markets

Chart 2: Impact on South African markets